Getting the right documents and finances in order is one of the most important steps a family can take to help Mom or Dad grow older safely and with dignity.

If you’re caring for an aging parent or family member, chances are you’ve already hit a moment where you needed a legal or financial detail and couldn’t find it. A doctor asks who the healthcare proxy is. A bill arrives for an account you didn’t know existed. On their own, these are small disruptions—but handled poorly, they become real stress at the worst possible time.

That’s why getting legal and financial affairs in order is one of the most powerful things a family can do. With a little guidance and some honest conversation, you may be surprised at how smooth and stress-free growing older can be—no matter what lies ahead. In this chapter we’ll walk through the essential documents, smart financial practices, and the sensitive conversations that make the difference.

“One of the most important documents you can have is a power of attorney. It’s comprehensive and gives your chosen designee the legal authority to make the decisions you would make if you were able.”

— Darren Mills, Esq., CPA · Trust & Estate Attorney

Legal Documents Every Family Needs

Power of Attorney (POA)

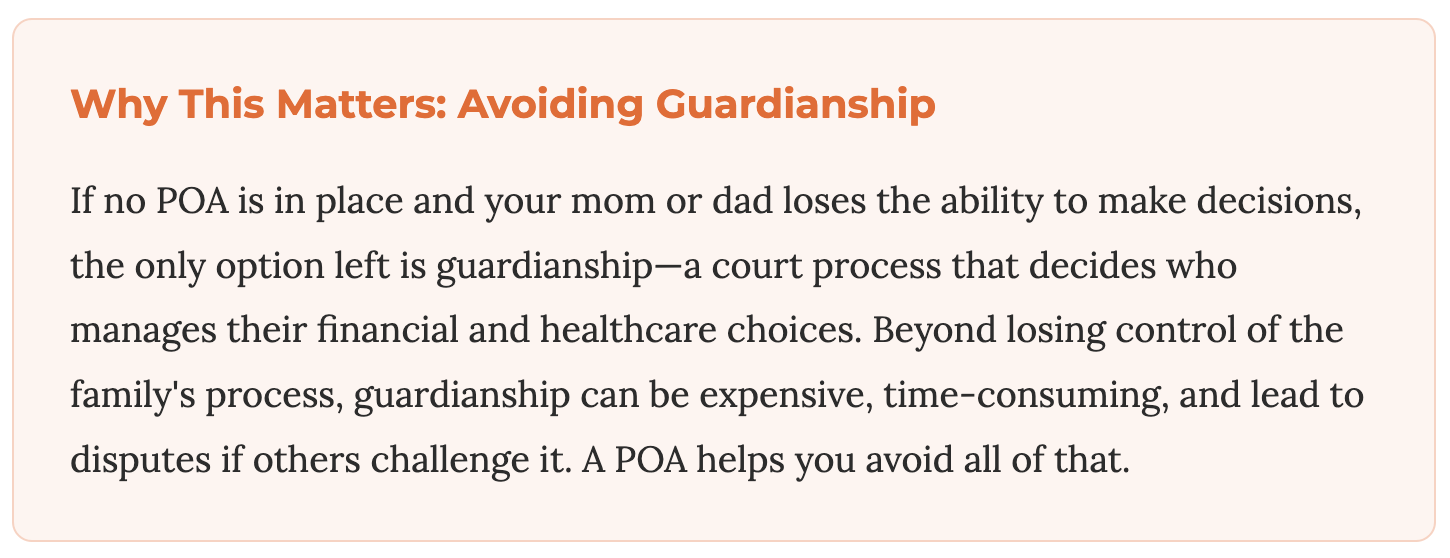

A POA grants another person the legal authority to act on your loved one’s behalf. It’s essential to name someone trusted—often a spouse, adult child, or close friend—and to review it periodically so it still reflects their wishes. There are two key types to understand:

- Financial durable POA — lets someone manage money, pay bills, file taxes, or sell property. “Durable” means it stays in effect even if the person becomes incapacitated.

- Medical POA (healthcare proxy) — lets someone make medical decisions if the individual can’t communicate their own wishes.

Healthcare Proxy vs. Medical Power of Attorney

These serve the same purpose—appointing someone to make medical decisions when the individual can’t—but terminology and scope vary by state. A healthcare proxy typically refers to the document itself and may be paired with a living will. A medical (or healthcare) POA is a broader term that can include added instructions, such as hospital transfers or specific treatments.

Advance Directives & Living Wills

An advance directive spells out a person’s preferences for medical care if they can’t communicate—often covering ventilators, feeding tubes, and resuscitation. Clear directives reduce family stress during emergencies. Some states, such as New Jersey, also offer a Practitioner’s Orders for Life-Sustaining Treatment, completed by the individual and their medical practitioner rather than an attorney. Depending on your state’s laws, you may also want to evaluate a Designation of Pre-Need Guardian.

Wills & Trusts

A will directs how assets and belongings are distributed after death and can name guardians for dependents. Without one, state law controls distribution—which may not match your loved one’s intentions. A will doesn’t avoid probate and becomes a public document upon death, so if you live in a state where probate is expensive and slow, asset titling and a trust should be part of the plan.

Trusts are revocable or irrevocable. A living (revocable) trust transfers ownership of assets while the person is alive, helping avoid probate and keep matters private; on death it becomes irrevocable. Important: revocable trusts won’t protect assets from long-term-care costs—if that’s a concern, speak with an elder law attorney about whether an irrevocable trust is right for your family.

HIPAA Authorization

Privacy laws prevent providers from releasing health information without consent. A HIPAA authorization lets designated family members or caregivers access critical medical information. Because HIPAA is federal law, this document applies in all 50 states.

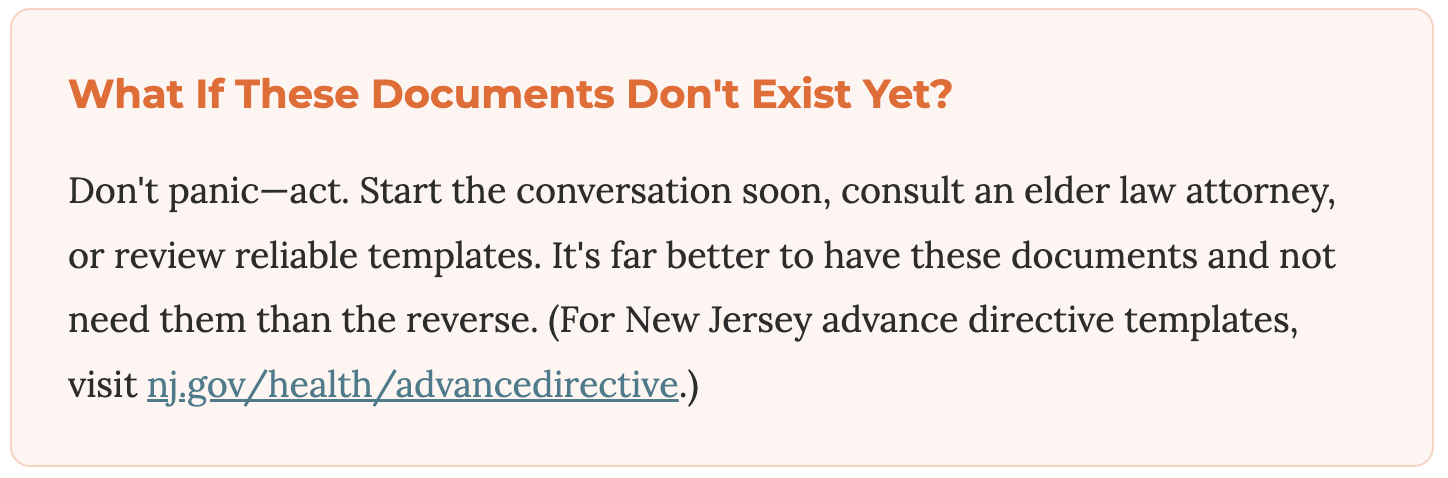

If You Move States

Moving doesn’t automatically mean your documents must be updated—but there may be good reasons to. Laws differ between states, and a third party in your new state may not accept an out-of-state power of attorney. The best practice is to consult a Trust & Estate Attorney wherever you now live.

Financial Organization for Peace of Mind

With the legal documents understood, the next step is making the maze of bills, accounts, and paperwork easier to manage. At Silver Solutions, we’ve helped thousands of families create safer, more organized, senior-friendly homes—and the same clarity applies to the financial picture.

Inventory Assets & Liabilities

One of the smartest first steps is building a comprehensive list, created together with your loved one:

- Bank accounts and credit cards

- Retirement accounts (IRAs, 401(k)s, pensions)

- Real estate, vehicles, and valuables

- Life insurance policies

- Debts, loans, and recurring bills

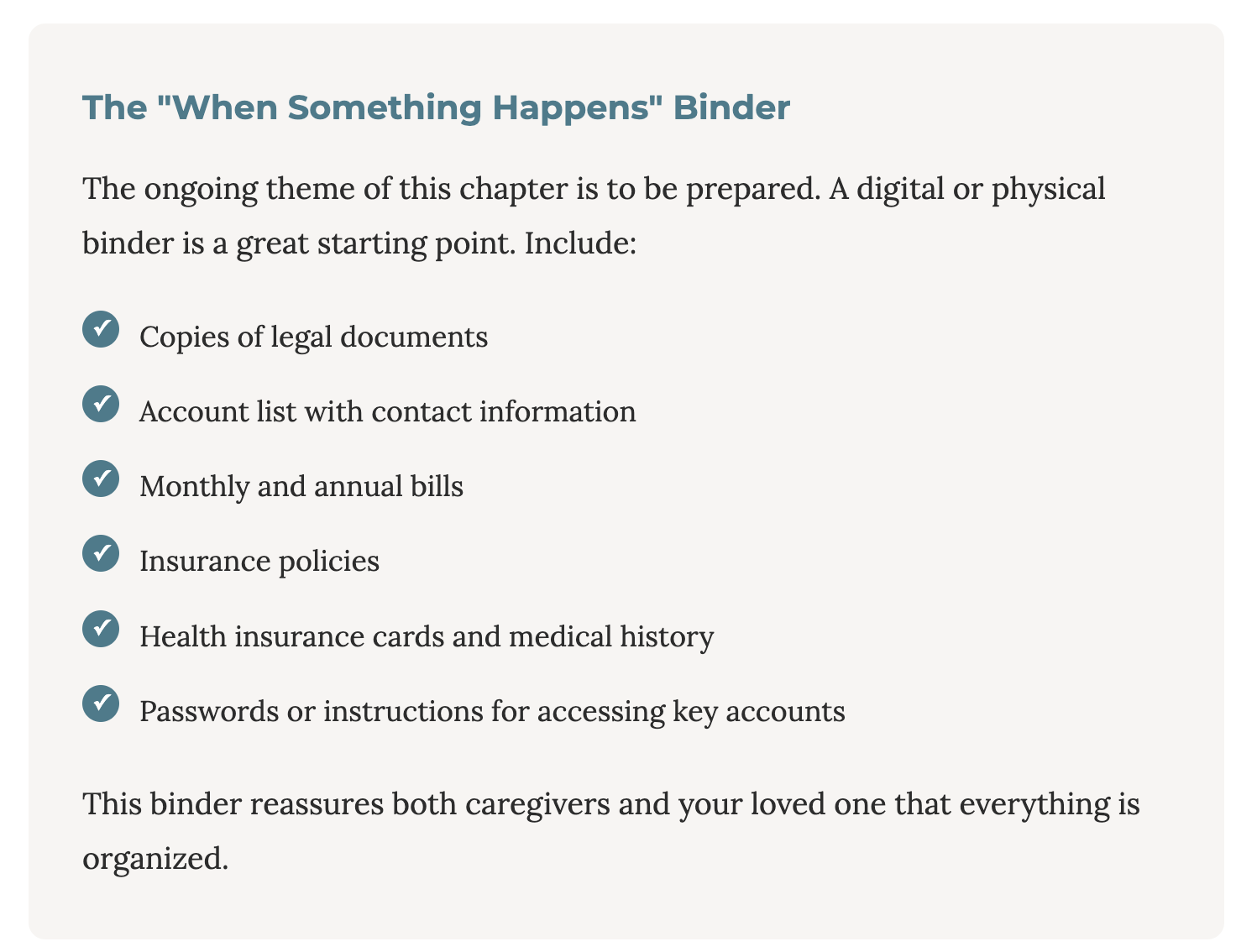

Having everything in one place prevents missed payments and overlooked assets, and eases future planning.

Who Knows Where the Money Is?

Avoid frantic, crisis-driven searches by making sure at least one trusted person understands the layout of your loved one’s financial life. They don’t need every detail—but they must know how to access critical information.

Digital Assets & Passwords

Make sure you or another trusted person can reach online banking, investment platforms, and health portals. Use a password manager or a secure written list.

Automated vs. Manual Payments

Mom or Dad may prefer paper checks—but if cognitive decline is a concern, automating payments helps avoid missed bills and late fees. If you go this route, keep them involved with a monthly statement review.

Estate Planning & Long-Term Wealth Protection

Estate planning benefits families at every income level—it minimizes confusion, reduces conflict, and ensures values are honored. Seek financial and legal counsel for complicated situations, but here’s a simple framework to start with:

- A will naming heirs and guardians

- A trust (when helpful) to distribute assets efficiently

- Durable POA and healthcare directive

- A letter of intent providing context and personal wishes

Remember that certain accounts—like IRAs and life insurance—pass directly to named beneficiaries, bypassing the will, so review those designations regularly.

Avoiding Family Conflict

- Be inclusive and transparent; share the broad plan while your parent is alive.

- Encourage a personal letter explaining decisions that may surprise or disappoint.

- Use neutral professionals—estate planners or mediators—when needed.

Other Helpful Tools & Resources

Long-Term Care Insurance

Covers a range of long-term care expenses, but coverage varies—so ask what services are covered and for how long, whether there are elimination periods or daily limits, and whether premiums can rise over time.

Senior-Specific Lenders

Providers like ElderLife Financial offer short-term loans for assisted living expenses or bridge funding during a home sale. Consult your advisor to see if it fits your situation.

Veterans’ Benefits & Government Assistance

Aid & Attendance (for qualified veterans and their spouses) can offset care costs, and programs like SNAP, LIHEAP, and local transport services may also help.

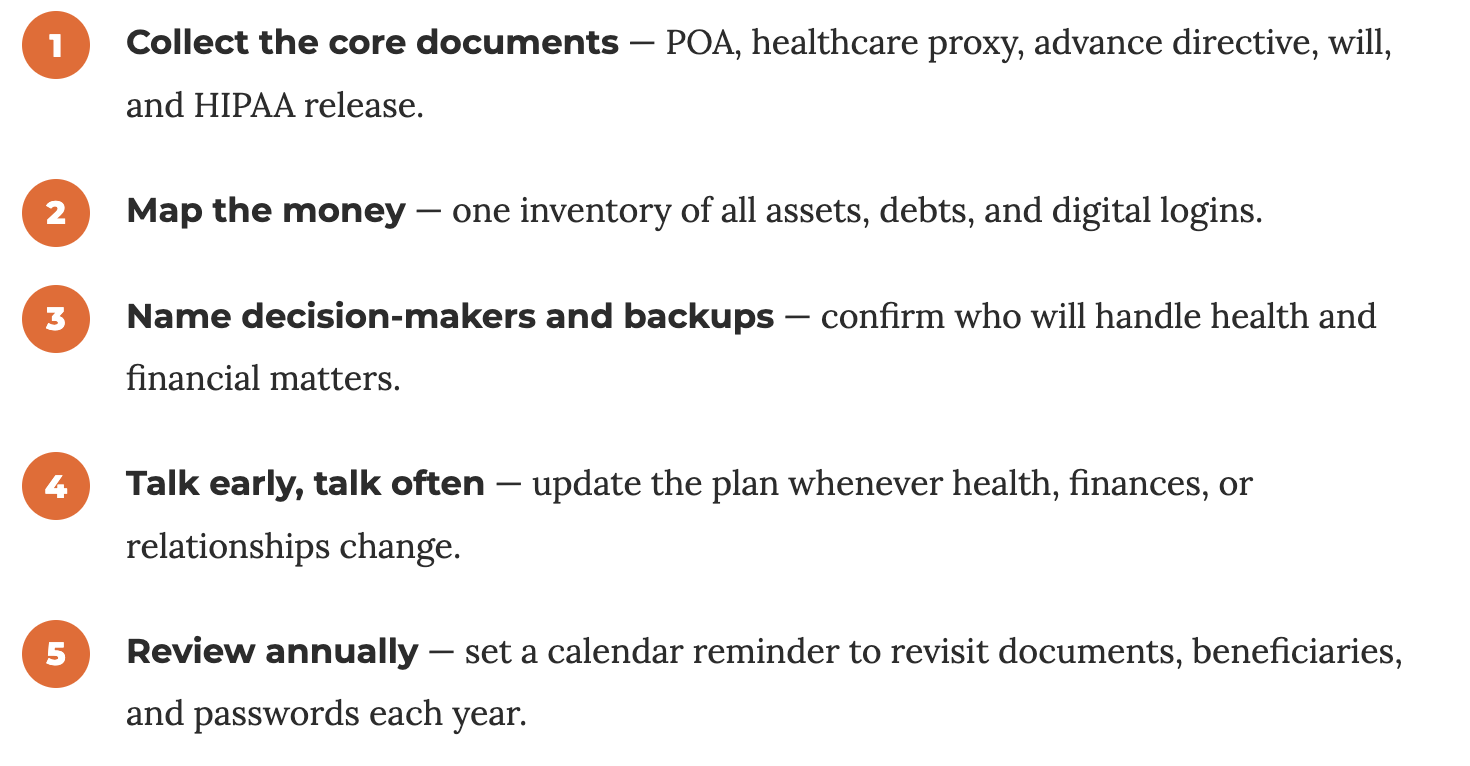

Pulling It All Together: A 5-Step Summary

One of the most common questions families ask us is, “How do I know it’s time?” The honest answer is: there’s rarely a single perfect moment. More often, multiple signs accumulate over time—some subtle, others sudden—that together point toward the need for a more structured environment.

Click or Call

Speak to a Specialist

You Don’t Have to Navigate This Alone

Getting affairs in order can feel overwhelming—there’s a lot to gather, and many of the conversations are emotional. But every step you take now is one less surprise later, and a little preparation goes a long way toward peace of mind.

At Silver Solutions, we’ve helped thousands of families bring clarity and structure to exactly these moments. While we’re not attorneys or financial advisors, we help families get organized, create senior-friendly homes, and build the kind of order that makes legal and financial planning far less daunting. We’re right here with you.

- Free, no-obligation consultations to help you build a plan

- Home organization and decluttering to centralize important documents

- Safe Living Solutions to keep your loved one secure while you plan ahead

- Safety365 ongoing virtual check-ins as needs change

Download the Full Age Wise Guide — Chapter 5

Get the complete Legal & Financial Essentials chapter as a PDF—including the documents checklist, the “When Something Happens” binder, and the 5-step action plan to reference anytime.